Most homeowners believe their mortgage is their biggest housing expense. In 2026, that belief is costing them thousands of dollars a year and most don't realize it until it is too late.

The real cost of homeownership in America has quietly crossed a threshold most financial advisors haven't updated their clients on. When you add property taxes, insurance premiums, routine maintenance, emergency repairs, and rising contractor labor rates, the average U.S. homeowner is spending $21,424 per year on top of their mortgage payment, according to data tracked by housing economists in early 2026.

This guide breaks down exactly where that money goes and what you can do to stop the financial bleeding before it starts.

Why Your Mortgage Payment Keeps Rising (Even With a Fixed Rate)

You signed for a fixed 30-year mortgage. Your payment shouldn't change, right?

Wrong and this surprises more homeowners than almost anything else.

The culprit is escrow creep. Your monthly mortgage payment includes an escrow portion that covers property taxes and homeowners insurance. Both of these have risen sharply since 2022. In high-cost states like California, Florida, and Texas, homeowners have seen their monthly escrow payments increase by $200–$450 in just two years with zero change to their interest rate.

In Texas alone, property tax reassessments in 2025–2026 pushed median annual bills above $5,800 for homes in the $300,000–$400,000 range. That's an escrow hit most families didn't budget for. For a full breakdown of what Texas homeowners are paying across repairs and taxes, see our Texas Home Repair Costs 2026 Guide.

What you should do: Request a new escrow analysis from your lender every 12 months. Don't wait for the annual statement by then, you're already short.

The Death of the 1% Rule in 2026

For decades financial planners told homeowners to budget 1% of their home's value annually for maintenance. On a $350,000 home, that's $3,500/year.

That number is now dangerously outdated.

Current data shows the realistic maintenance budget is closer to 1.5% to 3%, depending on your home's age, location, and climate exposure. Here is why:

Labor costs have surged. The skilled trades shortage in the U.S. has pushed contractor hourly rates to levels that outpace general inflation by 2–3x. You're not just paying more you are waiting longer, which turns small problems into expensive ones.

Material costs haven't normalized. While lumber prices pulled back from 2021 highs, roofing materials, copper pipe, and HVAC components remain significantly elevated versus pre-2020 baselines.

Climate-related damage is increasing. Homes in Florida, Texas, and the Southwest are seeing accelerated wear on roofing, foundations, and HVAC systems due to extreme heat cycles, flooding, and storm activity.

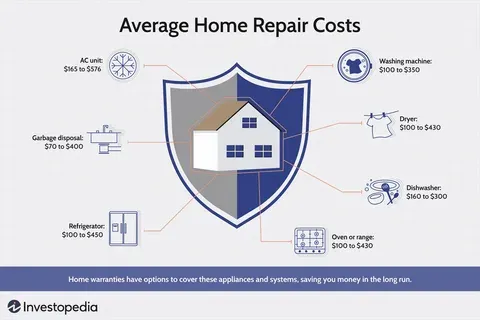

For a $400,000 home in a mid-cost U.S. city, you should realistically budget $6,000–$12,000/year for maintenance and unexpected repairs.

What Contractors Actually Charge Per Hour in 2026

This is the number homeowners almost never know until the invoice arrives.

Contractor Type | 2026 Avg. Hourly Rate | When You Typically Need Them |

|---|---|---|

General Contractor | $85 – $145 | Renovations, additions |

HVAC Technician | $90 – $160 | System repair, tune-ups |

Licensed Plumber | $95 – $175 | Leaks, pipe replacement |

Electrician | $100 – $185 | Wiring, panel upgrades |

Roofer | $75 – $130 | Leak repair, inspection |

Foundation Specialist | $100 – $200 | Crack repair, waterproofing |

These are national averages. In high-cost metros like New York City, San Francisco, and Boston, add 30–50% to these figures. NYC plumbing, for example, regularly runs $175–$250/hour for licensed work a reality that shocks homeowners who haven't called a plumber in five years. See our full NYC Plumbing Cost Guide 2026 for itemized pricing.

Why Repair Costs Are Rising Faster Than Inflation

The Consumer Price Index shows overall inflation moderating in 2025–2026. But home repair costs are not following that trend.

Three forces are driving this divergence:

Skilled labor shortage. The U.S. has an estimated shortfall of 500,000+ skilled tradespeople. With fewer qualified workers available, those who remain command premium rates and they're often booked out 2–6 weeks in advance. An HVAC failure in peak summer doesn't wait for your contractor's schedule.

Insurance-driven contractor pricing. As homeowners insurance companies tighten underwriting standards and drop coverage in high-risk states, contractors face higher liability insurance costs themselves. Those costs flow directly into your invoice.

Supply chain friction on parts. Specific components HVAC compressors, certain roofing materials, smart home hardware still face inconsistent supply, leading to markups. If your HVAC system needs a compressor replacement, you may find yourself choosing between a 3-week wait or paying a premium for expedited sourcing.

For homeowners deciding whether to repair or replace aging systems, the calculus has changed significantly. Our Repair vs. Replace HVAC Guide 2026 walks through the exact decision framework.

How Much Emergency Cash Homeowners Actually Need

Most financial advice says keep a 3–6 month emergency fund. For homeowners, that's not enough — because home emergencies are separate from personal income emergencies and they can happen simultaneously.

Here is the formula that actually works in 2026:

Home Emergency Reserve = (Home Value × 1.5%) + $3,000 buffer

On a $350,000 home, that's $5,250 + $3,000 = $8,250 in accessible cash, kept completely separate from your personal emergency fund.

What justifies that number? A single HVAC replacement runs $5,000–$12,000. A roof repair after storm damage can run $3,000–$8,000 before insurance kicks in. Foundation issues in Houston or Florida routinely start at $4,500 and go up fast.

If you're in a high-maintenance region Houston's foundation issues, Florida's storm exposure, Phoenix's extreme HVAC stress add another $2,000–$5,000 to your target reserve. See our Houston Foundation Repair Cost Guide and Florida Foundation Repair Guide for what regional homeowners are actually spending.

The Costs Homeowners Insurance Will NOT Cover

This is the section most homeowners skip until they file a claim and get a surprise denial.

Standard homeowners insurance policies in 2026 typically exclude:

Normal wear and tear. Your 20-year-old roof that finally fails isn't a covered "sudden event." Insurance companies are increasingly strict about age-related deterioration exclusions.

Flooding from ground water. Standard policies don't cover rising water from outside — only internal water damage (burst pipes, etc.). Flood insurance is a separate policy.

Foundation settling and movement. Unless caused by a covered peril like a burst pipe, foundation issues are almost always excluded. In Texas and Florida, this has become a major financial shock for homeowners.

HVAC neglect. If you haven't maintained your system and it fails, many policies won't cover the replacement. Maintenance records matter.

Sinkhole damage (in most states). Florida is unique in requiring sinkhole coverage, but most other states don't. If you own property in a sinkhole-prone area, check your policy carefully. Our Florida Sinkhole Damage Guide covers the warning signs every homeowner should know.

Understanding these gaps isn't pessimism it's how you plan a real budget instead of a fictional one.

How Local Costs Change Everything

National averages are a starting point. Where you live determines your actual number.

Texas homeowners face a specific triad of costs: foundation movement from expansive clay soil, extreme HVAC demand from heat, and high property tax burdens. Our Texas Home Repair 2026 Guide and Dallas HVAC Installation Guide cover the regional pricing in detail.

California homeowners are dealing with premium labor markets and strict permitting requirements that add 20–40% to almost any remodeling project. The Bay Area vs. LA cost gap is real and significant. See our California Home Remodeling Costs Guide.

Phoenix homeowners run HVAC systems harder than almost anywhere else in the country. A system that lasts 15 years in a mild climate may need replacement in 10–12 years in the Arizona heat. Our Phoenix HVAC Cost Guide explains the real replacement timeline and cost.

NYC homeowners and buyers face the country's highest contractor labor costs, combined with complex permitting and co-op/condo rules. Plumbing alone runs significantly above national averages.

2026 Homeowner Cost Survival Checklist

Use this to audit your financial exposure right now:

Calculate your correct maintenance reserve (home value × 1.5% + $3,000)

Separate home emergency fund from personal emergency fund

Review your homeowners insurance exclusions — specifically flood, foundation, and wear & tear

Get your HVAC system inspected before peak season (avoid emergency pricing)

Request an escrow analysis from your lender if payment has increased

Check your roof age — systems over 15 years old in storm-prone areas need inspection

Get at least 2 contractor quotes before any job over $1,500

Verify contractor licensing at your state contractor board before hiring

Data references: Bureau of Labor Statistics construction employment data, Zillow housing cost research, and regional contractor market surveys compiled through February 2026.